The distilled spirits tax credit is a

nonrefundable and

nontransferable credit that may be applied against income taxes imposed by KRS 141.020 (individual income tax) or KRS 141.040 (corporation income tax) and the limited liability entity tax (LLET) imposed by KRS 141.0401 for taxpayers who pay Kentucky property tax (ad valorem) on distilled spirits assessed under KRS 132.160 and timely paid under KRS 132.180. The amount of distilled spirits tax credit allowed is only for capital improvements at the premises of the licensed distiller. Unused credit amounts

cannot be carried forward to later tax years. However, the distilled spirits tax credit may be accumulated for multiple taxable years.

Application Process

The Schedule DS, Distilled Spirits Tax Credit, must be filed with the income tax return to determine the credit against the income tax liability and LLET liability for which the credit is claimed. The amount of the credit cannot exceed the amount of distilled spirits ad valorem tax paid during the period the capital improvements were made and completed. Supporting documentation including receipts, must be included with the return and records must be kept for five years.

The Schedule DS, Distilled Spirits Tax Credit, must be filed with the income tax return to determine the credit against the income tax liability and LLET liability for which the credit is claimed. The amount of the credit cannot exceed the amount of distilled spirits ad valorem tax paid during the period the capital improvements were made and completed. Supporting documentation including receipts, must be included with the return and records must be kept for five years.

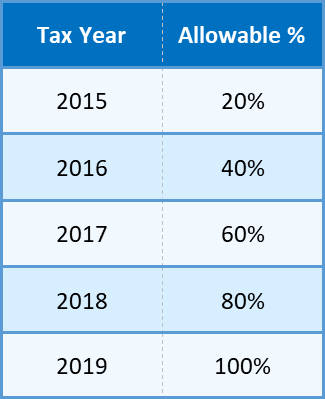

Phase-In Period The credit was phased in over five years. The table to the right shows the allowable credit percentage by tax year. The distilled spirits tax credit was fully phased in at 100% for tax years beginning on or after 1/1/2019.

Who Can Claim the Credit?

| Pass-through Entities

A pass-through entity (partnership, S-Corporation, LLC, general partnership, trust, etc.) may apply the distilled spirits tax credit against the LLET on its Kentucky Income and LLET Return and pass the credit through to its partners, members, or shareholders in the same proportion as the distributive share of income or loss is passed through with the ordering of the credits under KRS 141.0205.

The credit is passed through to the partners, members, or shareholders of a pass-through entity that are the partners, members, or shareholders at the time of the application and subsequent approval of the credit. The income is reported on the Kentucky Schedule K-1 and any credit that is passed through to the partners, members, or shareholders may be used against individual income tax or corporate income tax and LLET.

Individuals

A sole proprietor reporting business income on Schedule C (federal Form 1040) may claim the credit for distilled spirits under the business name. An individual may claim the credit if it is passed through to them from a partnership, LLC, or S-Corporation on a Kentucky Schedule K-1. An individual may also claim the credit if they timely filed and paid tangible property tax returns and tax liabilities, completed capital improvements on the premises of their distillery, and claimed the credit on the Schedule DS filed with their individual income tax return. If a husband and wife have both names listed on the schedule DS, the credit may be wholly claimed if they file jointly but must be split if they file separately. If the application lists only one of the spouse's names, the listed spouse is entitled to claim the full credit.

Corporations

A corporation may apply the distilled spirits tax credit against income tax and LLET on its Kentucky Corporation Income Tax and LLET Return. A corporation may also claim the credit if it is passed through to them from a pass-through entity on a Kentucky Schedule K-1.

|

Definition

Capital Improvement means any costs associated with:

(a) Construction, replacement, or remodeling of warehouses or facilities;

(b) Purchases of barrels and pallets used for the storage and aging of distilled spirits in maturing warehouses;

(c) Acquisition, construction, or installation of equipment for the use in the manufacture, bottling, or shipment of distilled spirits;

(d) Addition or replacement of access roads or parking facilities; and

(e) Construction, replacement, or remodeling of facilities to market or promote tourism, including but not limited to a visitor's center.