Forms Required

The Schedule INV is required to be completed and attached to the income tax return of the business that paid the tangible personal property (ad valorem) tax on the inventory. Taxpayers that receive a share of the inventory tax credit via a Kentucky K-1 through their ownership in a pass-through entity are not required to complete or attach the Schedule INV. Instead, the Schedule TCS for corporations and pass-through entities or Schedule ITC for individuals should be completed to reflect the taxpayer's share of the credit. The Schedule TCS or Schedule ITC is required to be attached to any return on which the credit is claimed. Links to these forms may be found on the right-hand side of this page.

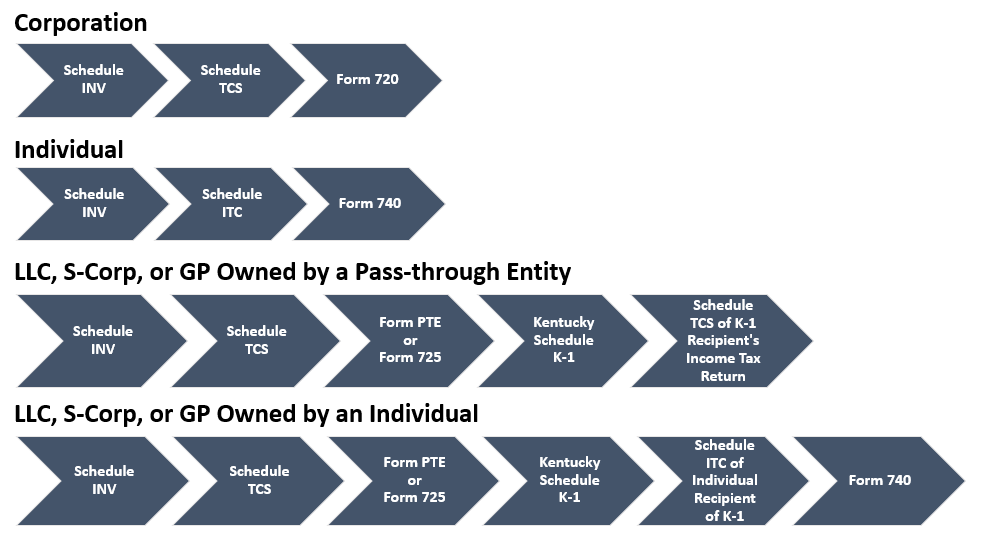

These flow charts show the progression of the tax credit through the applicable forms and schedules:

Fiscal Year Filers

Taxpayers that file on a fiscal-year basis should claim the credit based on the year in which the tax on inventory is timely paid. For example, if a corporation's tax year ends on June 30, 2019, and it timely pays ad valorem tax on inventory on December 20, 2018, it should claim an inventory tax credit of 25% on its 2018 return, because the ad valorem tax was paid between January 1, 2018 and December 31, 2018.

If a partnership has a fiscal year end date of September 30, 2020 and it timely pays ad valorem tax on inventory on December 20, 2019, then it should pass through 50% of the inventory tax credit to its partners on its 2019 return (fiscal year ended September 30, 2020), because the ad valorem tax was paid between January 1, 2019 and December 31, 2019.

|

Amended Tangible Personal Property Tax Returns

If you file an amended return and you receive an adjusted tax bill that was paid timely, use the amounts from the amended return. You should calculate the credit based only on the inventory values on which you ultimately paid tax. If you file an amended return after the payment due date, then the amount of tax paid late would not be eligible for the credit.

|

Centrally Assessed and Public Service Companies

Taxpayers filing Forms 61A200 or 61A800 should report inventory by the appropriate type of inventory listed (i.e. Merchant Inventory, Manufacturing Finished Goods, etc.) when completing lines 1 through 6 of the Schedule INV. Ignore the references to lines 31 through 36 of Form 62A500. Centrally Assessed and Public Service Companies may use the inventory tax credit calculator by inputting the inventory values on the appropriate lines of the calculator.

|